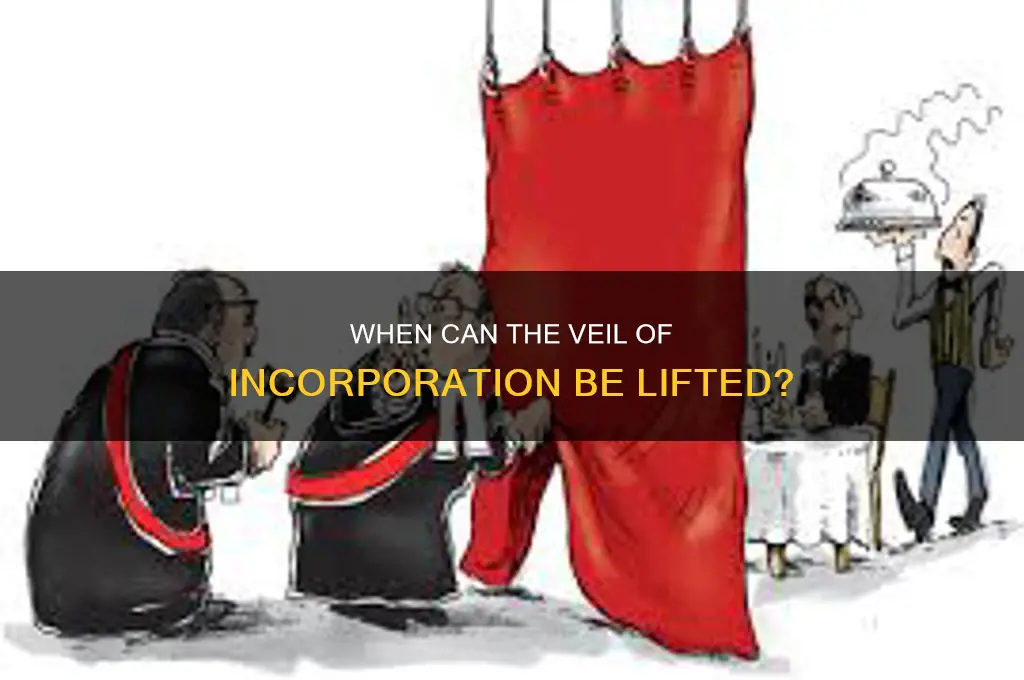

The veil of incorporation, a fundamental principle in corporate law, treats a company as a separate legal entity distinct from its shareholders, providing limited liability and protecting personal assets. However, under certain circumstances, courts may lift the veil to hold shareholders or directors personally liable for the company's actions. This typically occurs in cases of fraud, misuse of the corporate structure, undercapitalization, or where the company is deemed a mere facade for illegal activities. Additionally, specific statutory provisions may mandate piercing the veil in areas such as tax evasion, environmental violations, or non-compliance with regulatory requirements. Understanding when and why the veil can be lifted is crucial for businesses to ensure compliance and mitigate personal risks.

| Characteristics | Values |

|---|---|

| Fraud or Improper Conduct | The veil can be lifted if the company is used as a tool for fraud or illegal activities. |

| Agency or Trust Relationship | When a company acts as an agent or trustee, the veil may be lifted to reveal the principal or beneficiary. |

| Group Enterprises or Single Economic Unit | Courts may lift the veil if a group of companies operates as a single economic unit, disregarding corporate separateness. |

| Understatization or Evasion of Law | If a company is undercapitalized or used to evade legal obligations, the veil can be lifted. |

| Protection of Third-Party Rights | To protect third-party rights, such as creditors or employees, the veil may be lifted. |

| Tax Avoidance | In cases of aggressive tax avoidance schemes, the veil can be lifted to hold individuals accountable. |

| Environmental or Social Responsibility | Courts may lift the veil to enforce environmental or social responsibilities on individuals behind the company. |

| Public Interest or Justice | The veil can be lifted if maintaining it would defeat justice or harm the public interest. |

| Statutory Provisions | Specific laws or regulations may allow lifting the veil in certain circumstances (e.g., insolvency, labor laws). |

| Judicial Discretion | Courts have discretion to lift the veil based on the facts and equity of each case. |

Explore related products

What You'll Learn

![]()

Fraud or Improper Conduct

Fraudulent activities and improper conduct are among the most compelling reasons for courts to lift the corporate veil, exposing shareholders to personal liability. This legal action is not taken lightly, as it undermines the fundamental principle of limited liability that corporations are built upon. However, when a company is used as a vehicle for deceit or misconduct, the law steps in to prevent abuse and protect stakeholders. The doctrine of lifting the veil in such cases serves as a deterrent, ensuring that individuals cannot hide behind a corporate entity to perpetrate fraud or engage in unethical behavior.

Consider the scenario where a business owner establishes a company solely to defraud creditors. By transferring assets to the corporation while retaining personal control, the owner might attempt to shield themselves from debt obligations. Courts, however, are adept at recognizing such schemes. In *Jones v. Lipman* (1962), the House of Lords lifted the corporate veil when a seller created a company to evade a contract to sell property, demonstrating that fraudulent intent can nullify the protection of incorporation. This case underscores the principle that the corporate structure will not be allowed to facilitate injustice.

To avoid falling into this legal pitfall, business owners must ensure transparency and ethical conduct in all corporate dealings. For instance, maintaining clear records of transactions, avoiding commingling personal and corporate assets, and adhering to contractual obligations are essential practices. Small business owners, in particular, should be vigilant, as they often manage both personal and corporate finances closely. A practical tip is to consult legal counsel when structuring transactions to ensure compliance with laws and to mitigate the risk of the veil being lifted.

Comparatively, while some jurisdictions may require proof of explicit fraudulent intent, others may apply a broader standard of "improper conduct." For example, in certain U.S. states, courts may pierce the veil if a corporation is undercapitalized or fails to observe corporate formalities, even if fraud is not proven. This broader approach highlights the importance of adhering to corporate governance standards, regardless of the size or nature of the business. Entrepreneurs should treat their corporations as distinct entities, respecting formalities like holding regular board meetings and maintaining separate bank accounts.

In conclusion, fraud or improper conduct serves as a red flag for courts to scrutinize the corporate structure and potentially hold individuals accountable. The legal system’s willingness to lift the veil in such cases reinforces the principle that incorporation is a privilege, not a shield for wrongdoing. By understanding the triggers for this action and implementing proactive measures, business owners can safeguard their personal assets while upholding the integrity of their corporate endeavors.

Is Fashion Veiling Legally Required? Exploring Global Laws and Cultural Norms

You may want to see also

Explore related products

![]()

Undercapitalization and Insolvency

Undercapitalization often serves as a red flag for courts when considering whether to lift the corporate veil, particularly in cases where insolvency looms or has already occurred. When a company is established with insufficient capital to meet its obligations, it raises questions about the shareholders’ intent and the legitimacy of the corporate structure. Insolvency, in this context, becomes the tipping point that exposes the undercapitalization, revealing a potential abuse of the corporate form. For instance, if a company is incorporated with only $1,000 in capital but takes on liabilities of $1 million, creditors may argue that the shareholders used the corporation as a mere shield to avoid personal liability, rather than as a legitimate business entity.

Courts scrutinize undercapitalization as part of a broader inquiry into whether the corporation is a "sham" or merely an alter ego of its shareholders. In *Jones v. Henry (1984)*, the court emphasized that undercapitalization alone is not enough to pierce the veil but becomes significant when paired with other factors, such as insolvency or fraudulent intent. Practical examples include cases where directors continue trading despite knowing the company cannot pay its debts, a scenario often referred to as "insolvent trading." In such cases, shareholders may be held personally liable if the court determines the company was undercapitalized from the outset, indicating a disregard for corporate separateness.

To avoid the risk of the veil being lifted, companies must ensure adequate capitalization at incorporation and maintain sufficient reserves to meet foreseeable obligations. A rule of thumb is to capitalize the company with at least 50% of its projected first-year expenses, though this varies by industry and jurisdiction. For instance, a manufacturing company may require significantly more capital than a service-based business. Shareholders should also document their decision-making process, including capital contributions and risk assessments, to demonstrate good faith and compliance with legal obligations.

Creditors, on the other hand, can protect themselves by conducting due diligence before extending credit to undercapitalized entities. This includes reviewing financial statements, assessing the company’s capital structure, and requiring personal guarantees from shareholders when necessary. In jurisdictions like the UK, creditors can rely on statutory provisions such as the *Insolvency Act 1986*, which allows for director disqualification and personal liability in cases of wrongful trading. Similarly, in the U.S., courts may apply the "deepening insolvency" doctrine, holding shareholders accountable if their actions exacerbate the company’s financial distress.

Ultimately, undercapitalization and insolvency are intertwined issues that courts use to determine whether the corporate veil should be lifted. Shareholders must balance limited liability with the responsibility to ensure their company is adequately capitalized, while creditors must remain vigilant in assessing the financial health of their counterparts. By understanding these dynamics, both parties can mitigate risks and uphold the integrity of the corporate structure.

Pierce the Veil's Electrifying May 25 Setlist Revealed: Highlights & Surprises

You may want to see also

Explore related products

![]()

Agency or Alter Ego Doctrine

The Agency or Alter Ego Doctrine serves as a critical legal tool for piercing the corporate veil, allowing courts to hold individuals personally liable for corporate actions. This doctrine is invoked when a corporation is deemed a mere instrumentality or "alter ego" of its owner, often due to a failure to maintain corporate formalities or a commingling of personal and corporate assets. For instance, if a business owner uses a corporation solely to shield personal liabilities without adhering to legal distinctions, courts may disregard the corporate entity, exposing the owner to personal liability.

To apply this doctrine, courts typically examine specific factors, such as undercapitalization, disregard of corporate formalities, and the absence of separate financial records. For example, if a small business owner operates a company with insufficient funds to meet obligations and uses corporate accounts for personal expenses, a court might find grounds to lift the veil. Practical steps to avoid this include maintaining a dedicated business bank account, holding regular board meetings, and ensuring proper documentation of corporate decisions.

A comparative analysis reveals that the Alter Ego Doctrine is more stringent in jurisdictions like California, where courts require clear evidence of injustice or inequity before piercing the veil. In contrast, Delaware courts are more protective of corporate entities, demanding proof of fraud or wrongful intent. This variation underscores the importance of understanding local legal standards and tailoring corporate practices accordingly.

Persuasively, the Alter Ego Doctrine acts as a deterrent against abusive corporate practices, ensuring that business owners cannot exploit the corporate form to evade responsibility. However, it also poses risks for legitimate businesses that inadvertently fail to comply with formalities. To mitigate this, business owners should consult legal counsel to establish robust corporate governance structures and maintain clear separation between personal and corporate affairs.

In conclusion, the Agency or Alter Ego Doctrine is a powerful mechanism for holding individuals accountable when corporate protections are misused. By understanding its criteria and taking proactive measures, business owners can safeguard their personal assets while respecting the integrity of the corporate structure. This balance is essential for fostering trust in corporate entities while preventing abuse of legal protections.

Is the Wedding Veil Unveiled Filmed in Italy? Location Revealed

You may want to see also

Explore related products

![]()

Public Interest and Justice

The veil of incorporation, a fundamental principle in corporate law, shields shareholders from personal liability for a company's debts and actions. However, this protection is not absolute. In certain circumstances, courts will "lift the veil" and hold individuals accountable, particularly when public interest and justice demand it. This principle ensures that corporations cannot be used as tools for fraud, injustice, or activities that harm the wider community.

Public interest often dictates when the veil is lifted, especially in cases where a company's actions threaten public safety, health, or welfare. For instance, if a pharmaceutical company knowingly sells defective drugs, causing widespread harm, courts may pierce the corporate veil to hold individual directors or shareholders personally liable. This sends a strong message that corporate structures cannot shield those who endanger public well-being. Similarly, environmental disasters caused by corporate negligence often lead to veil-lifting, ensuring that those responsible face the consequences of their actions.

Justice, as a guiding principle, requires that the veil be lifted when a corporation is used as a mere facade to evade legal obligations or perpetrate fraud. For example, if a business owner transfers personal assets to a shell company to avoid paying creditors, courts will disregard the corporate entity and hold the individual accountable. This prevents the misuse of corporate structures to undermine fairness and equity in legal proceedings. The doctrine of "alter ego" is often applied here, where the corporation is so dominated by an individual that it loses its separate identity, justifying the lifting of the veil.

A comparative analysis reveals that jurisdictions differ in their approach to lifting the corporate veil, but the underlying rationale of protecting public interest and ensuring justice remains consistent. In the UK, the House of Lords in *Salomon v. Salomon & Co.* established the principle of corporate personality, but subsequent cases like *Gilford Motor Co. v. Horne* and *Jones v. Lipman* demonstrated that courts will intervene when justice requires it. In the U.S., the "instrumentality rule" and "enterprise liability" theories provide frameworks for piercing the veil, emphasizing the need to prevent abuse and protect stakeholders.

To navigate this complex area, businesses must adopt transparency and ethical practices. Practical tips include maintaining clear corporate records, ensuring proper capitalization, and avoiding commingling personal and corporate assets. Shareholders and directors should also be aware of their fiduciary duties and the potential consequences of neglecting them. For legal practitioners, understanding the nuances of veil-lifting doctrines across jurisdictions is crucial for advising clients effectively. Ultimately, the principle of lifting the corporate veil in the interest of public interest and justice serves as a vital check on corporate power, ensuring accountability and fairness in the business world.

Understanding the Walking Length Veil: A Bridal Accessory Guide

You may want to see also

Explore related products

![]()

Statutory Provisions and Exceptions

The veil of incorporation, a fundamental principle in corporate law, shields shareholders from personal liability for the company's debts and obligations. However, specific statutory provisions and exceptions allow this veil to be lifted, exposing shareholders to personal liability. These provisions are rooted in legislation and are designed to prevent abuse of the corporate structure, ensuring fairness and accountability.

Identifying Key Statutory Provisions

One prominent example is found in tax laws, where authorities may pierce the corporate veil if a company is deemed a "sham" or used solely for tax evasion. For instance, under the UK's Insolvency Act 1986, Section 213 empowers courts to hold directors personally liable if they are found guilty of wrongful trading. Similarly, in the U.S., the Internal Revenue Service (IRS) can disregard the corporate entity under 26 U.S.C. § 6901 if a corporation is used to circumvent tax obligations. These statutes provide clear frameworks for when the veil can be lifted, often requiring proof of fraudulent intent or significant wrongdoing.

Exceptions in Employment and Environmental Law

Beyond financial misconduct, statutory exceptions extend to employment and environmental regulations. In the EU, the Corporate Sustainability Reporting Directive (CSRD) mandates that large companies disclose environmental and social impacts, holding directors accountable for non-compliance. Similarly, under the U.S. Occupational Safety and Health Act (OSHA), corporate officers can be personally fined or imprisoned if they willfully violate workplace safety standards. These exceptions underscore the expanding scope of statutory provisions, reflecting societal demands for corporate responsibility.

Practical Considerations for Compliance

To avoid piercing the veil, companies must adhere to statutory requirements meticulously. This includes maintaining proper corporate records, ensuring financial transparency, and complying with industry-specific regulations. For instance, small business owners should be aware of the "alter ego" doctrine, often applied in state laws, which lifts the veil if the corporation is merely an extension of the owner’s personal affairs. Regular audits and legal consultations can mitigate risks, particularly in jurisdictions with stringent corporate governance laws.

Global Variations and Trends

Statutory provisions for lifting the veil vary significantly across jurisdictions, reflecting cultural and legal differences. In Germany, the GmbH law imposes strict capital maintenance rules, while in India, the Companies Act 2013 allows veil-lifting in cases of fraud or mismanagement. Globally, there is a growing trend toward harmonizing these provisions, as seen in the EU’s efforts to standardize corporate accountability. Businesses operating internationally must therefore navigate a complex web of laws, emphasizing the need for localized legal expertise.

While the veil of incorporation remains a cornerstone of corporate law, statutory provisions and exceptions ensure it is not a shield for misconduct. By understanding these laws and their applications, businesses can operate within legal boundaries while stakeholders can seek redress when necessary. The evolving nature of these provisions highlights the dynamic interplay between corporate autonomy and public interest.

Reviving Love: Should You Vow Renewal for Your Marriage?

You may want to see also

Frequently asked questions

The veil of incorporation is a legal concept that separates a company from its owners, treating the company as a distinct legal entity. It protects shareholders from personal liability for the company’s debts and actions. It is important because it encourages investment by limiting personal risk.

The veil of incorporation can be lifted in specific circumstances, such as when there is evidence of fraud, improper conduct, or when the company is used as a mere facade to evade legal obligations. Courts may also lift the veil in cases of undercapitalization or where the company is a sham or alter ego of its owners.

Yes, the veil can be lifted in cases of tax evasion if it is proven that the company structure was deliberately used to evade tax liabilities. Tax authorities and courts may disregard the corporate entity to hold the individuals behind it accountable.

No, the veil does not protect directors and shareholders in all situations. It can be lifted if they engage in wrongful acts, such as fraud, misuse of company funds, or failure to comply with legal requirements, making them personally liable.

Yes, the rules and criteria for lifting the veil of incorporation vary between jurisdictions. Some countries have stricter requirements, while others may apply the principle more broadly. It depends on local corporate laws and judicial precedents.