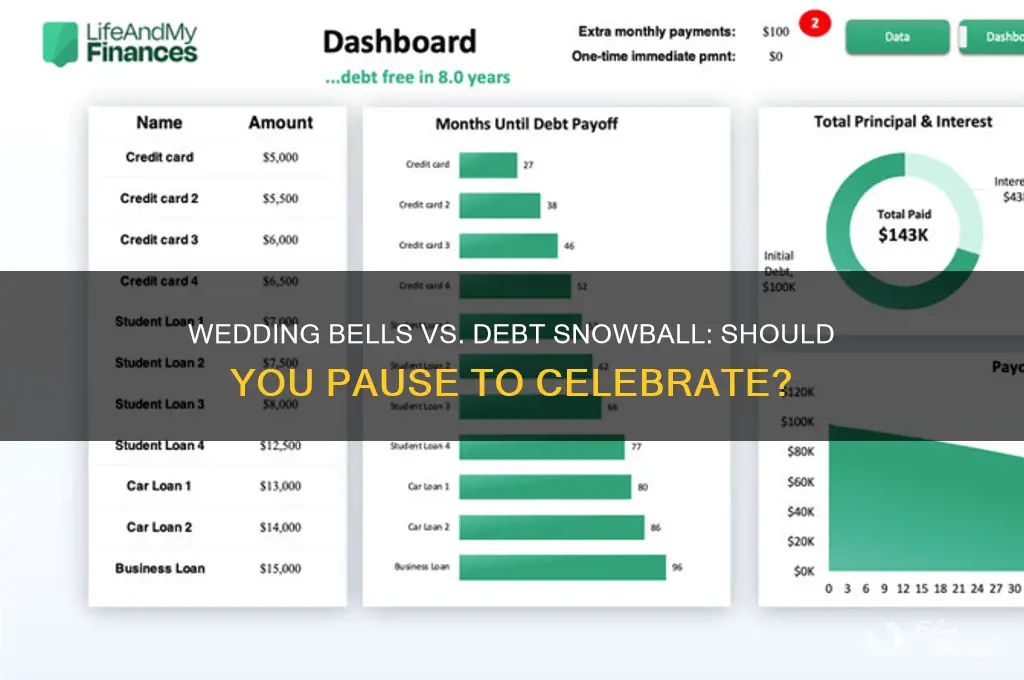

Deciding whether to pause a debt snowball strategy to fund a wedding is a significant financial decision that requires careful consideration. On one hand, sticking to the debt snowball method ensures consistent progress toward becoming debt-free, as it prioritizes paying off smaller debts first to build momentum. On the other hand, a wedding is a once-in-a-lifetime event that often comes with substantial costs, and delaying it might not be ideal. Balancing these priorities involves evaluating the urgency of debt repayment, the potential long-term impact of diverting funds, and whether there are alternative ways to finance the wedding without derailing your financial goals. Ultimately, the decision should align with your values, financial situation, and long-term objectives.

| Characteristics | Values |

|---|---|

| Financial Priority | Balancing debt repayment with life events like a wedding requires careful consideration. Prioritizing debt snowball (paying off smallest debts first) is generally recommended, but pausing temporarily for a wedding may be justified if it’s a one-time, meaningful expense. |

| Debt Snowball Progress | Pausing the debt snowball can slow momentum and increase interest costs over time. Assess how much progress has been made and the potential setback. |

| Wedding Cost | Average wedding costs in the U.S. range from $20,000 to $30,000 (2023 data). Evaluate if the expense is necessary or if it can be reduced. |

| Emergency Fund | Ensure an emergency fund (3-6 months of expenses) is in place before redirecting funds to a wedding to avoid financial strain. |

| Interest Rates | High-interest debt (e.g., credit cards) should be prioritized. Pausing repayment may increase overall debt burden due to accruing interest. |

| Timeframe | Consider the wedding timeline. If it’s far in the future, saving incrementally without pausing debt repayment may be feasible. |

| Emotional vs. Financial Impact | A wedding is emotionally significant, but long-term financial stability is crucial. Weigh the emotional value against the financial setback. |

| Alternative Funding | Explore options like family contributions, personal loans, or simplifying the wedding to avoid pausing debt repayment. |

| Long-Term Goals | Assess how pausing debt repayment affects long-term financial goals, such as buying a home or saving for retirement. |

| Budgeting | Create a detailed wedding budget to minimize overspending and determine if pausing debt repayment is truly necessary. |

| Psychological Impact | Debt can cause stress. Evaluate if pausing repayment for a wedding improves mental well-being or adds more stress in the long run. |

| Spousal Agreement | If marrying, discuss financial priorities and agree on whether pausing debt repayment aligns with shared goals. |

Explore related products

What You'll Learn

- Prioritizing Goals: Decide if wedding expenses outweigh debt repayment urgency in your financial plan

- Budgeting Strategies: Explore ways to fund the wedding without halting debt payments

- Opportunity Cost: Assess the long-term impact of pausing debt repayment for the wedding

- Emergency Funds: Ensure emergency savings are intact before reallocating funds for the wedding

- Debt Snowball Momentum: Consider how pausing might affect your motivation and progress in debt reduction

![]()

Prioritizing Goals: Decide if wedding expenses outweigh debt repayment urgency in your financial plan

When deciding whether to pause your debt snowball to fund wedding expenses, it’s crucial to prioritize your financial goals by evaluating the urgency of debt repayment versus the importance of your wedding. The debt snowball method, which focuses on paying off the smallest debts first to build momentum, is effective because it provides psychological wins and motivation. However, pausing this strategy to allocate funds to a wedding requires a careful assessment of your overall financial health and long-term objectives. Start by listing all your debts, their interest rates, and minimum payments, then compare this to your wedding budget. If your debts carry high interest rates, pausing repayment could lead to increased financial burden over time. Conversely, if the wedding is a non-negotiable priority, consider whether delaying it or scaling back expenses is a more viable option than disrupting your debt repayment plan.

Next, evaluate the emotional and financial significance of your wedding. For many, a wedding is a once-in-a-lifetime event that holds deep personal and cultural value. If this is the case for you, it may justify temporarily redirecting funds from debt repayment. However, ensure that the wedding expenses align with your long-term financial goals and do not derail your progress. Create a detailed wedding budget and explore cost-saving measures, such as DIY decorations, off-peak venue dates, or smaller guest lists. By minimizing wedding costs, you may be able to fund the event without significantly pausing your debt snowball. Additionally, consider whether family contributions or a side hustle could provide extra funds for the wedding, allowing you to maintain your debt repayment momentum.

Another critical factor is the impact of pausing debt repayment on your financial stability. If your debts are small and low-interest, a temporary pause might not have a substantial long-term effect. However, if you’re dealing with high-interest credit card debt or loans, pausing payments could result in accumulating more interest and prolonging your debt repayment timeline. Use a debt repayment calculator to estimate the additional costs of pausing your snowball and weigh them against the value of your wedding expenses. If the financial setback is minimal and the wedding is a priority, it may be a reasonable trade-off. Otherwise, consider alternative financing options, such as a low-interest personal loan for the wedding, to avoid disrupting your debt repayment plan.

Communication with your partner is essential in this decision-making process. Align on your shared financial priorities and discuss the potential trade-offs of pausing debt repayment for the wedding. If both parties agree that the wedding is worth the temporary financial shift, create a revised plan that balances both goals. This might involve accelerating debt repayment after the wedding or finding ways to cut costs in other areas of your budget. Remember, the goal is to make a decision that supports your financial well-being and relationship in the long run, rather than prioritizing one goal at the expense of the other.

Finally, consider the opportunity cost of your decision. Pausing your debt snowball for a wedding means delaying your journey to becoming debt-free, which could impact your ability to achieve other financial goals, such as saving for a home or investing for retirement. On the other hand, a wedding is a significant life event that may bring joy and strengthen relationships. Weigh the emotional and financial benefits of the wedding against the cost of slowing your debt repayment progress. If you decide to proceed, ensure you have a clear plan to resume and complete your debt snowball as soon as possible. By thoughtfully prioritizing your goals, you can make a decision that aligns with your values and financial aspirations.

A Memorable Greek Orthodox Wedding: How Long Does It Last?

You may want to see also

Explore related products

![]()

Budgeting Strategies: Explore ways to fund the wedding without halting debt payments

When considering whether to pause your debt snowball to fund a wedding, it’s essential to explore budgeting strategies that allow you to celebrate your special day without derailing your financial progress. The key is to find a balance between honoring your commitment to becoming debt-free and creating a memorable wedding. Start by prioritizing your budget and identifying areas where you can cut costs without sacrificing the essence of your celebration. Opt for a smaller guest list, choose an off-peak wedding date, or DIY certain elements like decorations or invitations. These adjustments can significantly reduce expenses while keeping your debt payments on track.

Another effective strategy is to create a dedicated wedding savings fund alongside your debt payments. Allocate a portion of your monthly income specifically for wedding expenses, ensuring it doesn’t interfere with your debt snowball. Consider increasing your income through side gigs, selling unused items, or taking on freelance work to boost your wedding fund. By treating wedding savings as a separate financial goal, you can avoid dipping into your debt repayment plan. This approach requires discipline but ensures you’re not sacrificing long-term financial health for short-term celebrations.

Leveraging low-cost or free resources can also help fund your wedding without pausing debt payments. Explore venues like public parks, community centers, or a family member’s backyard to save on rental fees. Use digital invitations instead of printed ones, and shop secondhand for decor or attire. Crowdsourcing talent from friends or family, such as a photographer or musician, can further reduce costs. These creative solutions allow you to have a beautiful wedding while maintaining your debt repayment momentum.

If you’re still short on funds, reconsider the scale and scope of your wedding. A smaller, intimate celebration can be just as meaningful and significantly more affordable. Focus on what truly matters—celebrating your love—rather than extravagant details. Additionally, avoid taking on new debt, such as wedding loans or high-interest credit card charges, as this could undo your progress on the debt snowball. Instead, stick to a cash-only budget for the wedding, ensuring you only spend what you’ve saved.

Finally, communicate openly with your partner about your financial priorities. Aligning on the importance of staying debt-free while planning a wedding fosters teamwork and shared goals. Together, brainstorm ways to cut costs or find alternative funding, such as contributions from family or a joint savings plan. By staying committed to your debt snowball and adopting these budgeting strategies, you can enjoy a beautiful wedding without compromising your financial future.

The Perfect Tan: Timing Your Pre-Wedding Glow

You may want to see also

Explore related products

![]()

Opportunity Cost: Assess the long-term impact of pausing debt repayment for the wedding

When considering whether to pause your debt snowball to fund a wedding, it’s crucial to evaluate the opportunity cost of this decision. Opportunity cost refers to the potential benefits you forgo by choosing one option over another. In this case, pausing debt repayment means losing the progress you’ve made in reducing your debt, which could have long-term financial implications. For example, if you’re paying off high-interest credit card debt, pausing repayment allows interest to continue accruing, increasing the total amount you’ll owe over time. This delay not only extends your debt repayment timeline but also reduces the funds available for future financial goals, such as saving for a home or retirement.

Another aspect of opportunity cost is the loss of momentum in your debt snowball strategy. The debt snowball method relies on psychological motivation as you pay off smaller debts first, building momentum to tackle larger ones. Pausing this process could disrupt your motivation and make it harder to resume focused debt repayment after the wedding. Additionally, if you redirect funds meant for debt repayment toward wedding expenses, you may find yourself relying on credit cards or loans to cover unexpected wedding costs, further exacerbating your debt situation. This creates a cycle where the wedding not only delays debt freedom but also potentially adds to your financial burden.

From a long-term financial health perspective, pausing debt repayment for a wedding could impact your credit score and overall financial stability. Higher debt balances and prolonged repayment periods can negatively affect your credit utilization ratio, which is a key factor in credit scoring. A lower credit score may limit your ability to secure favorable interest rates on future loans or credit cards, costing you more money in the long run. Furthermore, carrying debt for an extended period reduces your financial flexibility, making it harder to respond to emergencies or take advantage of investment opportunities.

It’s also important to consider the trade-off between experiences and financial goals. While a wedding is a significant life event, it’s essential to weigh its emotional and social value against the financial cost of delaying debt freedom. For instance, if becoming debt-free is a priority that aligns with your long-term financial plan, pausing repayment could set you back months or even years. On the other hand, if the wedding is non-negotiable, explore alternative ways to fund it without derailing your debt snowball, such as scaling down the event, increasing temporary income through side gigs, or using savings earmarked for other purposes.

Finally, assess the emotional and psychological impact of your decision. While a wedding is a memorable occasion, the stress of prolonged debt repayment can overshadow its joy. Financial stress is a significant contributor to anxiety and relationship strain, which could negate the positive experience of the wedding. Conversely, staying on track with your debt snowball may provide a sense of accomplishment and financial security that enhances your overall well-being. Carefully weigh these factors to make a decision that aligns with both your short-term desires and long-term financial objectives.

The Perfect Timing for Wedding Toasts: How Long Should They Be?

You may want to see also

Explore related products

![]()

Emergency Funds: Ensure emergency savings are intact before reallocating funds for the wedding

Before considering pausing your debt snowball to fund your wedding, it’s critical to prioritize your emergency fund. An emergency fund is your financial safety net, designed to cover unexpected expenses like medical bills, car repairs, or job loss. Without it, you risk derailing your financial stability and potentially relying on high-interest debt to cover emergencies. Do not reallocate emergency savings for discretionary expenses like a wedding, no matter how important the event feels. Your emergency fund should ideally cover 3-6 months of living expenses, and dipping into it for non-essential purposes leaves you vulnerable. Assess your current emergency savings and ensure they are fully intact before even considering redirecting other funds for the wedding.

If your emergency fund is already robust, evaluate whether pausing your debt snowball is truly necessary for the wedding. Many couples underestimate the power of budgeting and creativity in planning a wedding. Consider scaling back the event, negotiating vendor costs, or exploring DIY options to reduce expenses. By keeping your emergency fund untouched and finding ways to cut wedding costs, you can avoid disrupting your debt repayment progress. Remember, the goal of the debt snowball method is to build momentum and eliminate debt systematically; pausing it for non-essential expenses can delay your financial freedom.

Another key point is to distinguish between needs and wants. A wedding is a significant life event, but it’s a want, not a need. Emergency funds, on the other hand, are essential for financial security. Prioritizing a wedding over your emergency savings could force you to borrow money in a crisis, undoing the progress you’ve made on your debt snowball. Instead, explore alternative funding options for the wedding, such as saving specifically for it in advance, using a side hustle to generate extra income, or accepting contributions from family members. These approaches allow you to celebrate your wedding without compromising your financial safety net.

If you’re still tempted to use emergency funds, consider the long-term consequences. Pausing your debt snowball and depleting your emergency savings for a wedding can create a cycle of financial stress. Interest on paused debt continues to accrue, and without an emergency fund, you may end up relying on credit cards or loans for unexpected expenses. This not only slows your debt repayment but also increases the total cost of your debt. By keeping your emergency fund intact, you maintain financial flexibility and stay on track with your debt snowball, ensuring that your wedding doesn’t become a financial burden in the long run.

Finally, communicate openly with your partner about your financial priorities. Discuss the importance of maintaining an emergency fund and the potential risks of pausing your debt snowball. Aligning on these priorities can help you make a decision that supports both your short-term goals (like the wedding) and your long-term financial health. If you both agree to keep the emergency fund untouched, you can focus on finding creative ways to fund the wedding without sacrificing your financial security. Ultimately, a strong emergency fund and a commitment to your debt snowball will set the foundation for a financially stable marriage.

The Perfect Length for Wedding Vows: Personalized and Concise

You may want to see also

Explore related products

![ARTESORI Premium Wedding Vow Book for Her & Him, Soft Touch, Gold Foil, 28 Lined Pages, Wedding Vow Books His and Hers, Wedding Essentials, Wedding Registry Ideas, His and Hers Gifts [Ivory & Black]](https://m.media-amazon.com/images/I/71X4pKgPtNL._AC_UL320_.jpg)

![]()

Debt Snowball Momentum: Consider how pausing might affect your motivation and progress in debt reduction

When considering whether to pause your debt snowball to pay for a wedding, it’s crucial to evaluate how this decision might impact the momentum you’ve built in your debt reduction journey. The debt snowball method relies heavily on psychological wins—paying off smaller debts first to gain momentum and motivation. Pausing this process, even temporarily, could disrupt the sense of accomplishment that fuels your progress. Each small victory reinforces your commitment to becoming debt-free, and halting this progress might make it harder to regain focus once the wedding expenses are covered. Before making a decision, reflect on how much these psychological wins have driven your success so far.

Another factor to consider is the potential delay in reaching your debt-free goal. The debt snowball method is designed to be a structured, step-by-step process, and pausing it could extend the timeline for paying off your debts. For example, if you redirect funds meant for debt repayment toward wedding costs, you’re not only stopping progress but also potentially accruing more interest on existing debts. This could negate some of the gains you’ve made and slow down your overall progress. Ask yourself if delaying your debt-free goal is worth the immediate benefit of funding your wedding without additional loans.

Pausing your debt snowball might also create a mental loophole that makes it easier to justify future pauses or detours. Once you break the habit of consistent debt repayment, it can be challenging to reestablish it. The discipline required to stick to the debt snowball method is a critical part of its success, and interrupting this discipline could lead to a slippery slope. Consider whether pausing for a wedding might set a precedent for other expenses in the future, potentially derailing your financial goals entirely.

On the other hand, if you decide to pause, it’s essential to have a clear plan for resuming the debt snowball immediately after the wedding. Without a concrete strategy, the pause could turn into a prolonged hiatus, further damaging your momentum. Create a detailed timeline for getting back on track, including how much you’ll allocate to debt repayment post-wedding and which debts you’ll target first. This proactive approach can help minimize the negative impact on your progress and keep your long-term goals in sight.

Finally, weigh the emotional and financial value of the wedding against the cost of slowing your debt reduction. While a wedding is a significant life event, it’s important to balance this celebration with your financial priorities. If becoming debt-free is a top goal, consider whether there are ways to scale back wedding expenses or find alternative funding methods that don’t require pausing your debt snowball. Ultimately, preserving the momentum of your debt snowball is key to staying motivated and achieving financial freedom, so any decision should align with this overarching objective.

Obtaining a Wedding Certificate: A Quick Timeline

You may want to see also

Frequently asked questions

It depends on your financial situation and priorities. If the wedding is a top priority and you have a clear budget, you might temporarily pause the snowball to save for it. However, ensure you’re not accumulating new debt and resume paying off debt aggressively after the wedding.

Pausing the snowball temporarily may slow your debt repayment, but it doesn’t have to derail your progress entirely. Focus on minimizing wedding costs, avoiding new debt, and getting back to your debt repayment plan as soon as possible.

Create a detailed wedding budget, cut unnecessary expenses, and allocate a specific amount monthly for wedding savings. Continue making minimum payments on debts and prioritize the snowball method once wedding savings are complete.

Taking out a loan for the wedding is generally not recommended, as it adds to your debt burden. Instead, consider scaling down the wedding or extending the timeline to save without pausing your debt repayment plan.

Evaluate the emotional and financial value of the wedding versus the cost of delaying debt repayment. If the wedding is a non-negotiable priority and you have a plan to stay debt-free, it may be worth pausing temporarily. Otherwise, focus on paying off debt first.