Planning a wedding can be both exciting and financially daunting, but with a clear strategy and disciplined saving, it’s entirely possible to fund your dream celebration in three years. Start by setting a realistic budget that accounts for all expenses, from the venue to the honeymoon, and break it down into monthly savings goals. Consider opening a dedicated high-yield savings account to maximize interest earnings and keep your wedding fund separate from daily expenses. Explore ways to cut unnecessary costs in your current lifestyle, such as dining out less or canceling unused subscriptions, and redirect those savings toward your goal. Additionally, look for opportunities to increase your income, whether through side gigs, selling unused items, or negotiating a raise. Finally, track your progress regularly and celebrate small milestones to stay motivated, ensuring you’re on track to make your wedding day as magical as you’ve envisioned.

Explore related products

What You'll Learn

![]()

Set a Realistic Budget

Setting a realistic budget is the cornerstone of saving for a wedding in three years. Start by researching the average cost of weddings in your area, as expenses can vary significantly depending on location. Consider factors like venue, catering, attire, and entertainment to get a rough estimate. Once you have a baseline, discuss your priorities with your partner. Are you dreaming of a grand reception or would you rather allocate more funds to photography or a honeymoon? Identifying what matters most will help you allocate your budget effectively.

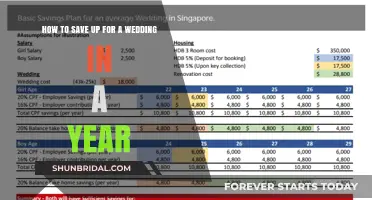

Next, break down your total estimated cost into monthly or yearly savings goals. For example, if your dream wedding costs $30,000, you’ll need to save approximately $833 per month over three years. Be honest about your current financial situation and adjust your expectations if necessary. It’s better to plan a wedding you can afford than to start your marriage burdened by debt. Use budgeting tools or apps to track your progress and ensure you’re staying on course.

Incorporate flexibility into your budget by setting aside a contingency fund for unexpected expenses. Weddings often come with surprises, whether it’s last-minute vendor changes or additional guest costs. Aim to save 5-10% of your total budget for these unforeseen expenses. This buffer will give you peace of mind and prevent overspending in other areas.

Finally, explore ways to reduce costs without compromising on your vision. Consider off-peak wedding dates, DIY decorations, or opting for a buffet-style meal instead of a plated dinner. Negotiate with vendors and look for package deals to maximize your budget. Remember, a realistic budget isn’t about cutting corners—it’s about making intentional choices that align with your priorities and financial capabilities.

Regularly review and adjust your budget as you save. Life circumstances can change, and staying adaptable will ensure you remain on track. Celebrate small milestones along the way to keep yourself motivated. By setting a realistic budget and sticking to it, you’ll not only save for your dream wedding but also build strong financial habits for your future together.

Your Guide to Officiating a Wedding in Georgia: Steps & Tips

You may want to see also

Explore related products

![]()

Automate Monthly Savings

Automating your monthly savings is a powerful strategy to ensure consistent progress toward your wedding fund goal. The key is to make saving effortless and systematic, so you’re not relying on willpower alone. Start by setting up an automatic transfer from your checking account to a dedicated wedding savings account. Most banks allow you to schedule recurring transfers, so choose a date shortly after your paycheck arrives to ensure the funds are available. Determine a realistic amount to save each month by calculating your monthly income, fixed expenses, and discretionary spending. Aim to save at least 10-15% of your monthly income, but adjust this based on your financial situation and wedding budget. The goal is to make the savings automatic, so you treat it like any other essential bill that must be paid.

To maximize your savings, consider using a high-yield savings account specifically for your wedding fund. These accounts typically offer higher interest rates than traditional savings accounts, allowing your money to grow faster over the three-year period. Once you’ve opened the account, link it to your checking account for seamless transfers. If your employer offers direct deposit, explore the option to split your paycheck and have a portion automatically deposited into your wedding savings account. This way, the money never hits your main account, reducing the temptation to spend it. Automation ensures that saving becomes a habit, not a choice, and helps you stay on track without constant reminders.

Another effective method is to use budgeting apps or financial tools that automate savings for you. Apps like Mint, Acorns, or Digit can analyze your spending patterns and automatically transfer small amounts into your savings account. Some apps even round up your purchases to the nearest dollar and save the difference. These tools are particularly useful if you struggle with manual savings or want to save additional funds without much effort. However, ensure the app you choose aligns with your financial goals and doesn’t charge excessive fees that could eat into your savings.

If you receive bonuses, tax refunds, or other windfalls, automate the process of saving a portion or all of it. Set up a rule that a certain percentage of any extra income goes directly into your wedding fund. For example, you could decide that 50% of your annual bonus or tax refund will be automatically transferred to your savings account. This prevents overspending and ensures that unexpected financial gains contribute to your long-term goal. Automation removes the hesitation or second-guessing that often comes with manual savings decisions.

Finally, regularly review and adjust your automated savings plan as your financial situation evolves. If you receive a raise, increase your monthly savings contribution to take advantage of the higher income. Similarly, if you pay off a significant debt, redirect those funds into your wedding savings. Life circumstances change, and your savings strategy should adapt accordingly. By automating your savings and periodically reassessing your plan, you’ll build a substantial wedding fund over three years without feeling overwhelmed or deprived. The key is consistency and leveraging automation to make saving a seamless part of your financial routine.

Crafting the Perfect Wedding Ceremony: A Sample Script Guide

You may want to see also

Explore related products

![]()

Cut Non-Essential Expenses

To effectively save for a wedding in three years, one of the most impactful strategies is to cut non-essential expenses. Start by evaluating your monthly spending to identify areas where you can reduce or eliminate costs. Begin with discretionary spending, such as dining out, entertainment, and subscription services. Cooking at home instead of eating at restaurants can save hundreds of dollars each month. Similarly, canceling unused gym memberships, streaming services, or magazines can free up additional funds. Track your expenses for a month to pinpoint where your money is going and prioritize needs over wants.

Next, reassess your daily habits to further cut non-essential expenses. Small, habitual purchases like daily coffee runs, snacks, or impulse buys can add up quickly. Opt for brewing coffee at home, packing lunches, and creating a shopping list to avoid unnecessary spending. If you enjoy hobbies or activities that require frequent purchases, look for cost-effective alternatives. For example, borrow books from the library instead of buying them, or explore free community events for entertainment. These minor adjustments can significantly increase your savings over time.

Another area to focus on is transportation and travel costs. If possible, reduce reliance on ride-sharing services or public transportation by carpooling, biking, or walking. For longer trips, consider staying with friends or family instead of booking hotels, or look for budget-friendly accommodations. Additionally, plan vacations strategically by traveling during off-peak seasons or using reward points to minimize expenses. By being mindful of how you spend on travel, you can redirect those funds toward your wedding savings.

Finally, evaluate your housing and utility expenses to identify opportunities to cut non-essential expenses. If you’re renting, consider downsizing to a smaller space or moving to a more affordable neighborhood. For homeowners, refinancing your mortgage or renting out a spare room could reduce monthly costs. Additionally, lower utility bills by adopting energy-efficient practices, such as using LED bulbs, unplugging devices when not in use, and adjusting thermostat settings. These changes not only save money but also contribute to a more sustainable lifestyle while you prepare for your wedding.

Recovering Your Deleted The Knot Wedding Website: A Step-by-Step Guide

You may want to see also

Explore related products

![]()

Explore Side Income Options

Saving for a wedding in three years is a realistic goal, especially if you explore side income options to boost your savings. One of the most effective ways to accelerate your wedding fund is by leveraging your skills and time to earn extra money. Start by identifying your strengths and interests—whether it’s writing, graphic design, photography, or tutoring—and turn them into freelance services. Platforms like Upwork, Fiverr, or Freelancer allow you to connect with clients globally and earn income on a flexible schedule. Even dedicating 10–15 hours a week to freelancing can significantly increase your savings over three years.

Another viable side income option is selling products or crafts online. If you’re creative, consider opening an Etsy shop to sell handmade items, digital downloads, or personalized gifts. Alternatively, you can flip items by purchasing them at a discount from thrift stores, garage sales, or clearance sections and reselling them on platforms like eBay or Facebook Marketplace. This requires some initial investment and research, but it can be highly profitable if done strategically. Focus on items in high demand, such as vintage clothing, furniture, or collectibles, to maximize your earnings.

For those who prefer a more hands-off approach, passive income streams like renting out assets can be a great option. If you have a spare room, list it on Airbnb to earn money from travelers. Similarly, renting out your car on platforms like Turo or your parking space on apps like JustPark can generate steady income with minimal effort. These options require some setup but can provide consistent cash flow over time, helping you reach your wedding savings goal faster.

If you enjoy pets or have a knack for physical tasks, consider offering pet-sitting, dog-walking, or handyman services in your local area. Websites like Rover or TaskRabbit make it easy to find clients and set your own rates. These gigs are flexible and can be tailored to fit your schedule, allowing you to earn extra money without interfering with your primary job. Additionally, seasonal opportunities like shoveling snow, mowing lawns, or decorating for holidays can provide short-term income boosts during specific times of the year.

Lastly, don’t overlook the potential of gig economy apps like Uber, DoorDash, or Instacart. These platforms offer immediate earning opportunities with no long-term commitment, making them ideal for supplementing your wedding savings. While the income may vary, consistency and peak-hour availability can maximize your earnings. Combine these gigs with other side income options to diversify your revenue streams and ensure steady progress toward your financial goal. By exploring these avenues, you can significantly increase your savings and make your dream wedding a reality in three years.

Understanding the Number of Processions in Traditional Wedding Ceremonies

You may want to see also

Explore related products

![]()

Track Progress Regularly

Tracking your progress regularly is essential when saving for a wedding over three years. It helps you stay motivated, identify areas for improvement, and ensure you’re on track to meet your financial goal. Start by setting up a dedicated savings account specifically for your wedding fund. This account should be separate from your everyday spending to avoid temptation and keep your savings focused. Use budgeting tools or apps that allow you to link your savings account and monitor your balance in real time. This visibility will remind you of your progress and keep your goal top of mind.

Next, establish a monthly or quarterly review process to assess your savings rate. At the end of each month, compare your actual savings to your target amount. For example, if your goal is to save $30,000 in three years, you’ll need to save approximately $833 per month. If you fall short one month, adjust your budget or find ways to cut expenses in the following months to make up the difference. Quarterly reviews are also useful for evaluating larger trends and making adjustments to your overall strategy if needed.

Utilize spreadsheets or financial tracking apps to log your savings progress and visualize your growth. Create a chart that shows your monthly contributions, total savings, and how close you are to your goal. This visual representation can be a powerful motivator and help you celebrate milestones along the way, such as reaching the 25% or 50% mark. Additionally, include a section in your spreadsheet for unexpected expenses or windfalls, so you can see how they impact your overall savings plan.

Regularly review your budget to ensure your savings plan remains realistic and achievable. Life circumstances can change—you might get a raise, face unexpected expenses, or decide to adjust your wedding plans. During your monthly or quarterly reviews, reassess your income, expenses, and savings rate to ensure they align with your current situation. If necessary, recalibrate your savings goal or timeline to stay on track without feeling overwhelmed.

Finally, involve your partner in the tracking process to maintain accountability and teamwork. Schedule joint check-ins to discuss your progress, celebrate successes, and brainstorm solutions for any challenges. This shared responsibility not only strengthens your financial partnership but also ensures both of you are committed to the savings plan. By tracking progress regularly together, you’ll stay focused, motivated, and aligned as you work toward your wedding savings goal.

Perfect Timing: When to Register for Your Dream Wedding Gifts

You may want to see also

Frequently asked questions

Determine your total wedding budget first, then divide it by 36 months. For example, if your budget is $30,000, aim to save approximately $833 per month. Adjust based on your income and expenses.

Use a dedicated savings account or a budgeting app to monitor your progress. Label the account specifically for wedding savings and review it monthly to ensure you’re on track.

Prioritize high-interest debt (like credit cards) first, as it can cost more in the long run. Once that’s under control, focus on building your wedding savings.

Yes! Consider DIY projects, off-peak wedding dates, and negotiating vendor prices. Also, look for ways to reduce everyday expenses, like cooking at home or cutting subscription services, to free up more money for savings.