Planning how to pay for a daughter's wedding can be both exciting and daunting, as it often involves balancing emotional significance with financial practicality. Weddings are significant life events, and the costs can quickly escalate, encompassing everything from the venue and catering to attire and entertainment. To navigate this, parents should start by setting a realistic budget, prioritizing what matters most to the couple, and exploring creative ways to save, such as DIY decorations or off-peak season dates. Additionally, considering contributions from both families, utilizing savings, or taking out a small loan can help manage expenses. Open communication with the couple about expectations and financial boundaries is essential to ensure the celebration remains meaningful without causing undue financial strain. Early planning and flexibility are key to creating a memorable wedding while staying within financial means.

| Characteristics | Values |

|---|---|

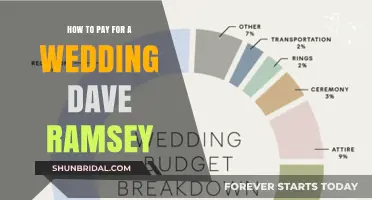

| Average Wedding Cost (US) | $30,000 (as of 2023, The Knot) |

| Parental Contribution | Traditionally, parents of the bride cover 45% of wedding costs |

| Popular Funding Methods | Savings, loans (personal/wedding), credit cards, crowdfunding, family contributions |

| Budgeting Tips | Prioritize must-haves, negotiate vendor contracts, DIY where possible, limit guest list |

| Financial Planning Tools | Wedding budgeting apps (e.g., WeddingWire, The Knot), spreadsheets |

| Tax Implications | Gifts to daughter/son-in-law up to $17,000 (2023 annual exclusion) are tax-free |

| Timeline | Start saving 2-3 years in advance, finalize budget 12-18 months before wedding |

| Alternative Options | Destination weddings (potentially cheaper), off-peak season discounts, all-inclusive venues |

| Communication | Discuss expectations and budget constraints early with daughter/couple |

| Emergency Fund | Allocate 5-10% of budget for unexpected expenses |

Explore related products

What You'll Learn

- Budget Planning: Determine total budget, prioritize expenses, and allocate funds for venue, catering, and decorations

- Savings Strategies: Start early, use high-yield savings, and consider wedding-specific savings accounts

- Family Contributions: Discuss financial support from extended family and clarify expectations for contributions

- Payment Options: Explore loans, credit cards, or crowdfunding platforms to cover additional costs

- Cost-Cutting Tips: Opt for off-peak dates, DIY decor, and negotiate vendor contracts for savings

![]()

Budget Planning: Determine total budget, prioritize expenses, and allocate funds for venue, catering, and decorations

When planning to pay for your daughter's wedding, budget planning is the cornerstone of ensuring a memorable event without financial strain. Start by determining the total budget you can comfortably allocate. Consider your savings, potential contributions from family members, and any financial assistance your daughter and her partner might provide. Be realistic about what you can afford to avoid unnecessary debt. Once the total budget is set, break it down into categories to ensure clarity and control over expenses.

Next, prioritize expenses based on what matters most to your daughter and the overall vision of the wedding. Typically, the venue, catering, and decorations are the largest expenses and should be allocated funds accordingly. Begin by researching average costs in your area for these items to set realistic expectations. For instance, the venue often consumes 40-50% of the total budget, while catering usually accounts for 25-35%. Decorations, though important, should be allocated a smaller portion, around 10-15%, unless it’s a top priority. Prioritizing ensures that funds are directed to the most critical aspects first.

When allocating funds for the venue, consider factors like guest count, location, and time of year, as these significantly impact costs. If the venue is a top priority, you may need to adjust other areas of the budget to accommodate it. For catering, decide whether a sit-down dinner, buffet, or cocktail-style reception aligns with your budget. Don’t forget to include costs for beverages, cake, and service staff. Decorations should enhance the atmosphere without overspending. Opt for cost-effective options like seasonal flowers, DIY centerpieces, or reusable decor items to stay within budget.

To maintain financial discipline, track expenses meticulously. Use spreadsheets or budgeting tools to monitor spending in each category and make adjustments as needed. If costs in one area exceed the allocated budget, reevaluate and cut back in less critical areas. For example, if the venue costs more than anticipated, consider simplifying the catering or decorations to balance the budget. Regularly reviewing the budget ensures you stay on track and avoid overspending.

Finally, consider contingency funds as part of your budget planning. Set aside 5-10% of the total budget for unexpected expenses, such as last-minute vendor changes or additional guests. This buffer provides peace of mind and flexibility to handle surprises without derailing your financial plan. By carefully determining the total budget, prioritizing expenses, and strategically allocating funds for the venue, catering, and decorations, you can create a beautiful wedding for your daughter while maintaining financial stability.

Open Bar Etiquette: How Long is Too Long?

You may want to see also

Explore related products

![]()

Savings Strategies: Start early, use high-yield savings, and consider wedding-specific savings accounts

Planning for your daughter's wedding financially is a thoughtful and proactive approach to ensure a memorable celebration without undue stress. One of the most effective savings strategies is to start early. The earlier you begin, the more time your savings have to grow, and the less pressure you’ll feel as the wedding date approaches. Treat wedding savings like any long-term financial goal—set a target amount based on estimated costs and break it down into monthly contributions. Starting early also allows you to take advantage of compound interest, which can significantly boost your savings over time.

Another key strategy is to use high-yield savings accounts. Traditional savings accounts often offer minimal interest rates, but high-yield savings accounts, money market accounts, or certificates of deposit (CDs) can provide higher returns. These accounts are low-risk and ensure your money grows faster than it would in a standard account. Compare interest rates, fees, and withdrawal restrictions to find the best option for your needs. By maximizing the growth of your savings, you’ll be better prepared to cover wedding expenses without dipping into other financial resources.

Consider opening a wedding-specific savings account to keep your funds organized and dedicated solely to the wedding. This not only helps you track progress but also prevents the temptation to use the money for other purposes. Some banks offer specialized accounts for life events like weddings, which may come with additional benefits or incentives. Labeling the account clearly as "Daughter's Wedding Fund" can also serve as a motivational reminder of your goal.

To further enhance your savings, automate your contributions. Set up regular transfers from your checking account to your high-yield or wedding-specific savings account. Automating savings ensures consistency and removes the need to remember manual contributions. Even small, consistent amounts can add up significantly over time, especially when combined with higher interest rates.

Finally, periodically review and adjust your savings plan as needed. Life circumstances, economic conditions, or wedding plans may change, requiring flexibility in your approach. If possible, increase contributions during periods of higher income or reduce non-essential expenses to allocate more funds to the wedding savings. Staying proactive and adaptable will help you stay on track to fund your daughter's wedding comfortably.

Weddings and Receptions: How Long Should You Plan For?

You may want to see also

Explore related products

![]()

Family Contributions: Discuss financial support from extended family and clarify expectations for contributions

When planning how to pay for your daughter's wedding, one of the most effective strategies is to explore family contributions from extended relatives. Weddings are often a communal celebration, and many families come together to share the financial burden. Start by identifying key family members who may be willing and able to contribute, such as grandparents, aunts, uncles, or even close cousins. Initiate open and honest conversations about the wedding plans and the associated costs. Be transparent about the budget and where additional support would be most helpful, whether it’s for the venue, catering, or other significant expenses.

Clarifying expectations for contributions is crucial to avoid misunderstandings or resentment later on. During discussions, ask family members directly if they are willing to contribute and, if so, how much they feel comfortable giving. Some relatives may prefer to cover specific aspects of the wedding, such as the rehearsal dinner or the wedding cake, rather than providing a lump sum. Document these agreements informally or formally, depending on the family dynamics, to ensure everyone is on the same page. It’s also important to express gratitude for their support, regardless of the amount, to foster a positive and collaborative atmosphere.

If extended family members are hesitant to contribute financially, consider alternative ways they can support the wedding. For example, a family member with a large property might offer their home as a venue, or someone with creative skills could assist with decorations or invitations. These non-monetary contributions can significantly reduce costs while still involving the family in meaningful ways. The key is to approach these conversations with flexibility and appreciation for whatever assistance they can provide.

In some families, cultural or traditional norms may dictate specific roles or contributions from extended relatives. For instance, in certain cultures, the bride’s family covers specific expenses, while the groom’s family handles others. Understanding and respecting these traditions can guide your discussions and ensure everyone feels included. However, it’s essential to adapt these traditions to fit the modern circumstances and financial realities of all involved parties.

Finally, manage expectations by setting a clear timeline for when contributions are needed. Wedding expenses often require upfront payments, so knowing when funds will be available helps with planning. If a family member commits to a contribution but is unable to provide it by the required date, be prepared to adjust the budget or explore alternative funding options. Open communication and realistic planning will ensure that family contributions enhance the wedding experience rather than causing stress.

Chelsea Clinton's Wedding Funding: Separating Fact from Fiction

You may want to see also

Explore related products

![]()

Payment Options: Explore loans, credit cards, or crowdfunding platforms to cover additional costs

When considering how to pay for your daughter’s wedding, exploring payment options like loans, credit cards, or crowdfunding platforms can help cover additional costs that may exceed your savings. Loans are a common choice for financing large events like weddings. Personal loans, often unsecured, can provide a lump sum with fixed interest rates and repayment terms. Before applying, compare lenders to find the best rates and terms. Secured loans, such as home equity loans or lines of credit, may offer lower interest rates but require collateral, which could be risky if repayment becomes difficult. Ensure you understand the total cost, including interest and fees, and have a clear repayment plan to avoid long-term financial strain.

Credit cards are another option, especially if you need flexibility or want to earn rewards. Many credit cards offer 0% APR introductory periods, which can be advantageous if you can pay off the balance before the promotional period ends. However, high interest rates apply afterward, so this option is best for short-term financing. Consider using a credit card for specific expenses, like venue deposits or vendor payments, rather than the entire wedding cost. Additionally, monitor your credit limit and avoid maxing out your card, as this can negatively impact your credit score.

Crowdfunding platforms have become a popular way to offset wedding expenses. Platforms like GoFundMe, Kickstarter, or specialized wedding crowdfunding sites allow you to share your story and request financial contributions from friends, family, and even acquaintances. To maximize success, create a compelling campaign with clear details about the wedding, why you’re crowdfunding, and how funds will be used. Offer small tokens of appreciation, like thank-you notes or personalized updates, to contributors. While crowdfunding can be effective, it’s important to approach it with sensitivity, as not everyone may feel comfortable contributing.

Combining these payment options can also be a strategic approach. For example, you might use a personal loan to cover the majority of costs while relying on a credit card for smaller, unexpected expenses. Alternatively, crowdfunding could supplement other financing methods, reducing the overall amount you need to borrow or charge. Whichever options you choose, prioritize transparency with your daughter and partner about the financial plan to ensure everyone is on the same page.

Before committing to any payment option, assess your financial situation carefully. Calculate the total wedding budget, including potential overruns, and determine how much you can realistically afford to borrow or repay. Consulting a financial advisor can provide tailored guidance based on your circumstances. Remember, while loans, credit cards, and crowdfunding can help cover costs, they should be used thoughtfully to avoid long-term financial stress and ensure your daughter’s wedding remains a joyous occasion rather than a financial burden.

RSVP Etiquette: Wedding Guest Response Timing

You may want to see also

Explore related products

![]()

Cost-Cutting Tips: Opt for off-peak dates, DIY decor, and negotiate vendor contracts for savings

When planning your daughter’s wedding, one of the most effective cost-cutting strategies is to opt for off-peak dates. Wedding venues and vendors often charge premium rates during peak seasons, such as summer and early fall. By choosing a date in the off-season, like winter or early spring, you can significantly reduce costs. Additionally, consider hosting the wedding on a weekday instead of a weekend, as venues and vendors are typically less in demand and more willing to offer discounts. This simple shift in timing can save you thousands of dollars without compromising the quality of the celebration.

Another powerful way to cut costs is to embrace DIY decor. Instead of hiring a professional decorator, get creative and personalize the wedding decor yourself. Pinterest and YouTube are excellent resources for inspiration and tutorials. Simple yet elegant ideas include crafting centerpieces from mason jars and fresh flowers, creating handmade signage, or designing unique table settings. Involve family and friends in the process to make it a fun, collaborative effort. Not only will this save money, but it will also add a heartfelt, personal touch to the wedding. Just be sure to start early to avoid last-minute stress.

Negotiating vendor contracts is a crucial step in maximizing savings. Many vendors, including caterers, photographers, and florists, are open to negotiation, especially if you’re flexible with their services. For example, ask if they offer package deals, discounts for off-peak dates, or if they can reduce costs by customizing their services to fit your budget. Don’t be afraid to shop around and compare quotes from multiple vendors to ensure you’re getting the best deal. Polite persistence and clear communication can lead to significant savings without sacrificing quality.

Combining these strategies—opting for off-peak dates, DIY decor, and negotiating vendor contracts—can dramatically reduce the overall cost of your daughter’s wedding. By being strategic with timing, taking a hands-on approach to decor, and leveraging negotiation skills, you can create a beautiful and memorable wedding while staying within your budget. Remember, the key is to prioritize what truly matters and find creative ways to save without compromising the essence of the celebration. With careful planning and a bit of ingenuity, you can make your daughter’s special day both affordable and unforgettable.

Smart Wedding Planning: Strategies to Dodge the Hidden Wedding Tax

You may want to see also

Frequently asked questions

Begin by setting a realistic budget, opening a dedicated savings account, and contributing regularly. Consider automating your savings to ensure consistency.

Explore options like crowdfunding, taking out a low-interest personal loan, or using a home equity line of credit (HELOC) if you own property.

Yes, involving them helps set clear expectations and ensures everyone is aligned on the budget and priorities.

Focus on must-haves like venue, catering, and photography, and allocate funds accordingly. Be willing to cut back on less essential items.

Generally, no, as weddings are considered personal expenses. However, gifting money to your daughter may have gift tax implications if it exceeds annual exclusion limits.