During his 2016 presidential campaign, Donald Trump repeatedly promised to release his tax returns if elected, a pledge that aligned with decades of precedent set by previous candidates. However, after winning the election, Trump reversed course, citing ongoing audits by the IRS as a reason to withhold the documents, despite no legal barrier to their release. This reversal sparked widespread criticism and speculation about what the returns might reveal regarding his finances, business dealings, and potential conflicts of interest. The issue became a focal point of scrutiny throughout his presidency, with critics accusing him of breaking a key campaign promise and undermining transparency in government.

| Characteristics | Values |

|---|---|

| Promise Made | During his 2016 presidential campaign, Trump vowed to release his tax returns. |

| Reason for Promise | To maintain transparency and follow tradition set by previous presidents. |

| Fulfillment of Promise | Trump did not release his tax returns during his presidency. |

| Excuses Given | Cited ongoing IRS audit as the primary reason for not releasing them. |

| Legal Requirement | There is no legal requirement for presidents to release tax returns, but it is a long-standing norm. |

| Public Reaction | Critics accused Trump of hiding potential conflicts of interest or financial irregularities. |

| Media Coverage | Extensive media scrutiny and speculation about Trump's finances. |

| Legal Battles | Trump fought legal battles to keep his tax returns private, including lawsuits against Congress and state prosecutors. |

| Partial Disclosure | Some financial information was released during congressional investigations, but full tax returns remained undisclosed. |

| Impact on Legacy | Trump's refusal to release tax returns remains a point of controversy in his political legacy. |

Explore related products

What You'll Learn

- Trump's Campaign Promise: Pledged to release tax returns after election, citing audit completion

- Audit Excuse: Claimed ongoing IRS audit prevented release, despite no legal barrier

- Legal Battles: Courts ordered release, but Trump fought subpoenas and delayed disclosure

- Public Pressure: Critics demanded transparency, questioning hidden financial conflicts or foreign ties

- Unfulfilled Vow: Never released full tax returns during presidency, breaking his promise

![]()

Trump's Campaign Promise: Pledged to release tax returns after election, citing audit completion

During his 2016 presidential campaign, Donald Trump repeatedly promised to release his tax returns once an ongoing audit by the IRS was completed. This pledge was a direct response to growing public and media scrutiny over his financial transparency, a standard practice for presidential candidates since the 1970s. Trump’s assurance hinged on the audit as a legal and procedural barrier, suggesting that disclosure would follow its resolution. This commitment became a cornerstone of his campaign’s credibility, particularly as he positioned himself as a self-made billionaire with nothing to hide. However, the promise was never fulfilled, leaving a trail of unanswered questions about his finances, business dealings, and potential conflicts of interest.

Analyzing Trump’s rationale, the audit excuse raises critical questions about the relationship between IRS procedures and public disclosure. The IRS itself has clarified that audits do not prohibit individuals from releasing their tax returns voluntarily. This fact undermines Trump’s justification and suggests that the audit was a convenient pretext rather than a legal impediment. By framing the issue as a procedural delay, Trump effectively sidestepped immediate scrutiny while maintaining the appearance of compliance. This tactic highlights a broader strategy of leveraging technicalities to manage public perception, a pattern observed in other areas of his political and business career.

From a practical standpoint, the unfulfilled promise has significant implications for transparency in American politics. Tax returns provide critical insights into a candidate’s financial health, potential foreign entanglements, and adherence to tax laws. For voters, this information is essential for making informed decisions. Trump’s refusal to release his returns set a precedent that could embolden future candidates to withhold similar information, eroding a decades-long norm. This shift risks normalizing opacity in leadership, undermining public trust, and weakening accountability mechanisms in government.

Comparatively, Trump’s stance contrasts sharply with his predecessors and successors. Every major-party presidential nominee since 1980 has released their tax returns, often years’ worth, to demonstrate financial integrity. Even when facing audits, figures like Richard Nixon released partial returns to maintain public trust. Trump’s deviation from this norm underscores a deliberate break from established ethical standards. This comparison not only highlights his uniqueness but also raises concerns about the long-term impact on electoral transparency and the expectations voters should have of their leaders.

In conclusion, Trump’s campaign promise to release his tax returns after an audit was a strategic commitment that ultimately went unfulfilled. This broken pledge reveals a calculated approach to managing public scrutiny, leveraging procedural excuses to avoid transparency. The fallout from this decision extends beyond Trump’s presidency, challenging the norms of accountability and setting a potentially dangerous precedent for future leaders. As voters and observers, understanding this episode underscores the importance of demanding consistent transparency from those seeking public office, regardless of their excuses.

Can Ordained Ministers Renew Vows? A Comprehensive Guide for Couples

You may want to see also

Explore related products

![]()

Audit Excuse: Claimed ongoing IRS audit prevented release, despite no legal barrier

Donald Trump's refusal to release his tax returns during his presidential campaigns was marked by a recurring excuse: an ongoing IRS audit. This claim, however, was misleading at best. IRS guidelines explicitly state that individuals are free to release their tax returns even while under audit. There is no legal barrier to transparency in this scenario, yet Trump persistently used the audit as a shield, raising questions about his true motivations.

Example: In 2016, Trump stated, "I'm being audited now... I will release them as soon as the audit is finished." This promise remained unfulfilled throughout his presidency, despite audits typically concluding within a few years.

The audit excuse served as a strategic deflection, allowing Trump to avoid scrutiny of his financial dealings. By invoking the audit, he created the illusion of legitimacy for his secrecy, exploiting public unfamiliarity with IRS policies. This tactic effectively shifted the narrative from his potential conflicts of interest to a bureaucratic process, buying him time and deflecting pressure to disclose. Analysis: Trump's reliance on this excuse highlights a calculated effort to control the narrative around his finances. It demonstrates a willingness to prioritize personal interests over transparency, a cornerstone of public trust in elected officials.

Takeaway: Understanding the audit excuse reveals a deliberate strategy to obfuscate financial information. It underscores the importance of fact-checking political claims and demanding accountability, especially when transparency is legally feasible.

To counter such tactics, voters must be informed about their rights to information and the limitations of audit confidentiality. Steps: 1. Familiarize yourself with IRS policies on tax return disclosure during audits. 2. Question politicians who use audits as a reason for withholding financial information. 3. Support legislation that mandates transparency, such as requiring presidential candidates to release tax returns. Cautions: Be wary of politicians who exploit procedural technicalities to avoid accountability. Remember, audits are a routine part of the tax system and should not be a barrier to transparency. Conclusion: The audit excuse is a red herring, a distraction from the real issue of financial transparency. By understanding this tactic, voters can better hold their leaders accountable and ensure that public trust is not undermined by misleading claims.

Monastics and the Bodhisattva Vow: Exploring Commitment and Practice

You may want to see also

Explore related products

![TurboTax Desktop Deluxe 2025, Federal & State Tax Return [PC/Mac Download]](https://m.media-amazon.com/images/I/71uOJaU7UvL._AC_UY218_.jpg)

![]()

Legal Battles: Courts ordered release, but Trump fought subpoenas and delayed disclosure

During his 2016 presidential campaign, Donald Trump repeatedly promised to release his tax returns, a standard practice for presidential candidates to ensure transparency. However, once elected, he broke this vow, citing ongoing audits as a reason for withholding them. This reversal sparked intense scrutiny and legal challenges, as critics and investigators sought to uncover potential conflicts of interest, financial improprieties, or foreign entanglements. The resulting legal battles became a defining feature of Trump’s presidency, with courts ordering the release of his tax records, only to be met with relentless resistance through subpoenas and delays.

The first major legal confrontation arose in 2019 when the House Ways and Means Committee subpoenaed Trump’s tax returns from the Treasury Department, citing a federal law allowing such requests. Trump’s legal team countered by arguing that the subpoena was politically motivated and lacked a legitimate legislative purpose. This set off a protracted court battle, with Trump’s attorneys employing procedural tactics to stall the process. Despite a 2020 Supreme Court ruling that presidents are not immune from subpoenas, Trump continued to fight, appealing lower court decisions and exploiting legal loopholes to delay disclosure. This strategy effectively kept his tax returns hidden throughout his presidency.

Simultaneously, New York prosecutors launched a criminal investigation into Trump’s business dealings, seeking his tax records as part of their inquiry. In 2021, the Supreme Court rejected Trump’s claim of absolute immunity, paving the way for Manhattan District Attorney Cyrus Vance Jr. to obtain the documents. Yet, even after this defeat, Trump’s legal team filed additional motions, arguing that the subpoena was overly broad and intrusive. These efforts, while ultimately unsuccessful, further delayed the release of the records, underscoring Trump’s determination to shield his finances from public view.

The legal battles over Trump’s tax returns highlight a broader tension between executive privilege and the public’s right to transparency. While courts consistently ruled in favor of disclosure, Trump’s aggressive litigation strategy exploited the slow pace of the judicial system, effectively delaying accountability. This case study serves as a cautionary tale about the limits of legal mechanisms in enforcing transparency, particularly when faced with a determined adversary willing to weaponize procedural delays. For future administrations, it underscores the need for stronger legislative safeguards to prevent such obstruction.

Practically, these legal battles offer lessons for investigators and lawmakers. First, anticipate and prepare for protracted litigation by allocating resources for legal challenges. Second, craft subpoenas with precision to withstand claims of overbreadth or political motivation. Finally, consider legislative reforms to streamline the process of obtaining presidential financial records, reducing opportunities for delay. While Trump’s tax returns were eventually released in 2022, the years of legal wrangling demonstrate the fragility of transparency norms in the face of strategic obstruction.

Skipping Wedding Vows: Is It Possible or a Tradition to Keep?

You may want to see also

Explore related products

![TurboTax Desktop Premier 2025, Federal & State Tax Return [PC/Mac Download]](https://m.media-amazon.com/images/I/71RgxnEm-tL._AC_UY218_.jpg)

![TurboTax Desktop Home & Business 2025, Federal & State Tax Return [PC/Mac Download]](https://m.media-amazon.com/images/I/71KOcfYElCL._AC_UY218_.jpg)

![[OLD VERSION] TurboTax Deluxe 2024 Tax Software, Federal & State Tax Return [PC/MAC Download]](https://m.media-amazon.com/images/I/71UbHaUeeUL._AC_UY218_.jpg)

![TurboTax Desktop Deluxe 2025, Federal Tax Return [PC/Mac Download]](https://m.media-amazon.com/images/I/71zRbfw0RdL._AC_UY218_.jpg)

![TurboTax Desktop Business 2025, Federal Tax Return [PC Download]](https://m.media-amazon.com/images/I/71UL+5xLOeL._AC_UY218_.jpg)

![]()

Public Pressure: Critics demanded transparency, questioning hidden financial conflicts or foreign ties

During his 2016 presidential campaign, Donald Trump repeatedly promised to release his tax returns, a standard practice for candidates to demonstrate financial transparency. However, once elected, he broke this vow, citing ongoing audits as a reason for withholding them. This reversal sparked intense public pressure, with critics demanding accountability and questioning what Trump might be hiding. The focus shifted from a procedural expectation to a deeper concern: were there undisclosed financial conflicts or foreign ties that could compromise his presidency?

The call for transparency was not merely symbolic. Tax returns provide a window into a public official’s financial dealings, revealing potential conflicts of interest, sources of income, and ties to foreign entities. Critics argued that Trump’s refusal to release his returns left the public in the dark about his business entanglements, particularly his global real estate empire. For instance, questions arose about whether his companies had financial obligations to foreign banks or governments that could influence U.S. policy decisions. Without access to his tax records, these concerns remained unverifiable, fueling suspicion and eroding trust.

Public pressure mounted as watchdog groups, journalists, and political opponents framed Trump’s secrecy as a threat to democratic norms. Protests, petitions, and media investigations highlighted the precedent set by previous presidents, who had voluntarily disclosed their finances. The issue became a rallying cry for transparency advocates, who argued that voters deserved to know whether their leader’s personal interests aligned with the nation’s. Legal battles ensued, with congressional committees and state prosecutors seeking access to Trump’s tax records, underscoring the urgency of the matter.

The debate over Trump’s tax returns also exposed broader systemic issues. It raised questions about the adequacy of existing laws requiring financial disclosures from public officials. Critics called for stronger enforcement mechanisms and penalties for non-compliance, emphasizing that transparency should not be optional. Practical steps, such as mandating the release of tax returns for all presidential candidates, were proposed to prevent future controversies. This push for reform reflected a growing public demand for accountability in an era of increasing political polarization.

In retrospect, the public pressure on Trump to release his tax returns was more than a political skirmish—it was a battle over the principles of openness and integrity in governance. By refusing to disclose his finances, Trump not only broke a campaign promise but also fueled doubts about his commitment to serving the public interest. The episode serves as a cautionary tale, reminding us that transparency is not just a bureaucratic formality but a cornerstone of trust between leaders and the people they serve.

Did Samson Violate His Nazirite Vow by Touching the Lion?

You may want to see also

Explore related products

![(Old Version) H&R Block Tax Software Deluxe + State 2024 with Refund Bonus Offer (Amazon Exclusive) Win/Mac [PC/Mac Online Code]](https://m.media-amazon.com/images/I/51+fonAXhPL._AC_UY218_.jpg)

![[OLD VERSION] TurboTax Home & Business 2024 Tax Software, Federal & State Tax Return [PC/MAC Download]](https://m.media-amazon.com/images/I/71b5aAzdXOL._AC_UY218_.jpg)

![]()

Unfulfilled Vow: Never released full tax returns during presidency, breaking his promise

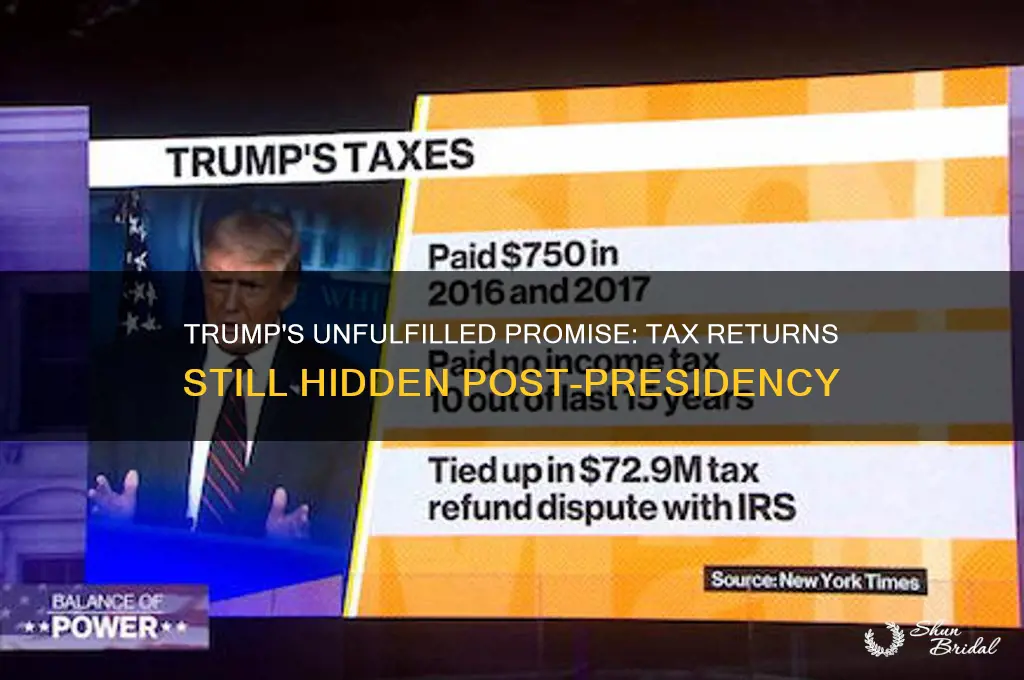

Donald Trump's refusal to release his full tax returns during his presidency stands as a stark example of a broken campaign promise, one that eroded public trust and set a concerning precedent. Despite repeatedly vowing to disclose his financial records if elected, Trump consistently cited ongoing audits as a reason for withholding them, a justification that lacked legal basis. The IRS itself confirmed that audits do not prohibit individuals from sharing their tax information, yet Trump remained steadfast in his secrecy. This unfulfilled vow not only contradicted decades of presidential transparency but also fueled speculation about potential conflicts of interest, foreign entanglements, and the extent of his wealth—or lack thereof.

Analyzing the implications of this broken promise reveals a deeper issue: the normalization of opacity in leadership. By disregarding the tradition of tax disclosure, Trump undermined a key mechanism for holding public officials accountable. Tax returns provide critical insights into a leader's financial health, potential biases, and adherence to tax laws. Without this transparency, citizens are left to rely on speculation and leaks, as seen in the 2016 and 2017 revelations by *The New York Times*, which exposed years of tax avoidance and questionable business practices. Trump's actions effectively weakened the norm of financial disclosure, leaving future administrations with a dangerous precedent to follow.

From a practical standpoint, Trump's refusal to release his tax returns highlights the need for stronger legislative safeguards. While the Presidential Tax Transparency Act, introduced in 2019, aimed to mandate tax disclosure for presidential candidates, it failed to gain traction. Advocates for transparency argue that such measures are essential to prevent conflicts of interest and ensure public trust. For instance, requiring candidates to release at least 10 years of tax returns, as proposed in the bill, could provide a comprehensive view of their financial history. Until such laws are enacted, the onus remains on voters to demand accountability and on the media to investigate and expose inconsistencies.

Comparatively, Trump's stance on tax transparency starkly contrasts with that of his predecessors. Every president since Richard Nixon had voluntarily released their tax returns, recognizing it as a duty to the American people. Trump's deviation from this norm raises questions about his motivations. Was it a strategic move to hide financial vulnerabilities, or a deliberate attempt to challenge established norms? Regardless, the impact is clear: his actions diminished the expectation of transparency, leaving a void that future leaders may exploit. This erosion of trust is not merely a political footnote but a warning about the fragility of democratic norms.

In conclusion, Trump's unfulfilled vow to release his tax returns is more than a broken promise—it’s a symptom of a broader retreat from accountability. By prioritizing secrecy over transparency, he not only betrayed his campaign pledge but also weakened the mechanisms that ensure leaders act in the public interest. Moving forward, this episode underscores the urgent need for legislative action and public vigilance to restore and strengthen the norms of financial disclosure. Without such measures, the promise of transparency risks becoming an empty gesture, leaving citizens in the dark about the financial dealings of those who lead them.

Trump's Medicaid Promise: Fact-Checking His Vow to Not Cut Benefits

You may want to see also

Frequently asked questions

Yes, during his 2016 presidential campaign, Donald Trump repeatedly stated he would release his tax returns once elected, pending the completion of a routine audit by the IRS.

Trump never released his full tax returns, citing ongoing IRS audits as the reason. Critics argued that audits do not legally prevent the release of tax returns, and many viewed his refusal as a broken campaign promise.

Yes, in 2021, *The New York Times* published extensive details from Trump’s tax records, revealing significant financial losses and minimal tax payments over several years. However, these were obtained through investigative reporting, not voluntarily released by Trump.